Interest Rate Swaps: Our latest article, Swaps and Basis Trades Warn Of Mounting Liquidity Problems, touched on adverse rate of interest swap spreads as an omen of potential liquidity issues. To remain on the subject of liquidity, we didn’t present a lot element about swaps. Nor did we talk about their significance to the monetary system. Accordingly, we ended the dialogue as follows:

Given the complexity of rate of interest swaps and their significance to the plumbing of the whole monetary system, we are going to talk about them additional in a coming article.

Shockingly, on condition that we thought readers would discover rate of interest swaps boring or wonky to most readers, now we have obtained a couple of emails asking for extra data. Given the significance of liquidity to all markets and the way rate of interest swap spreads are an excellent liquidity barometer, it’s price providing you with that “coming article” now.

The Curiosity Charge Swap Markets

For individuals who didn’t learn our prior article, we share context concerning the dimension of the rate of interest swap markets.

For a correct framework, the approximate whole market cap of the U.S. inventory market is $50 trillion, and the worldwide inventory market, together with the U.S., is about double that. Moreover, the worldwide bond market is roughly $133 trillion.

As proven under, the notional worth of all excellent rate of interest swaps is roughly $575 trillion or greater than double the mixed worth of the worldwide bond and inventory markets!

Interest Rate Swaps: What Are Curiosity Charge Swaps?

Interest Rate Swaps: Rate of interest swaps are by-product contracts through which two counterparties conform to swap a sequence of money flows over a set schedule for an outlined time period.

Mostly, one celebration agrees to make periodic funds at a set rate of interest and, in return, receives floating-rate funds. The counterparty receives the mounted funds and pays the floating charge.

Sellers quote rate of interest swaps as both the yield on the mounted charge aspect of the settlement or the distinction between the mounted charge yield and that of an equal length U.S. Treasury bond. The latter, which is extra frequent, is named the swap unfold.

The floating-rate leg is often based mostly on the day by day Secured In a single day Financing Charge (SOFR). SOFR, the latest alternative for LIBOR, is the rate of interest banks pay or obtain from one another to borrow or lend cash in a single day, with U.S. Treasury securities serving as collateral. As a result of US Treasury belongings safe such in a single day borrowing, SOFR is actually a risk-free in a single day rate of interest. SOFR usually trades barely under the Fed’s focused Fed Funds charge. Fed Funds are unsecured in a single day loans between banks; thus, they contain some credit score threat.

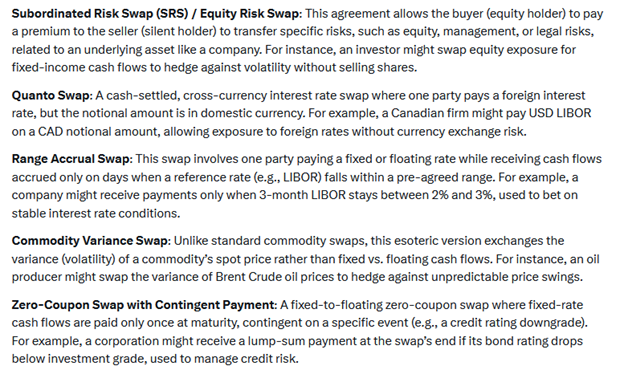

It’s price sharing that there are various different kinds of swap contracts. Listed here are a couple of of the extra advanced agreements, courtesy of Grok.

Interest Rate Swaps: Digging In Deeper

To higher admire a “plain vanilla” rate of interest swap contract, we analyze a hypothetical ten-year annual paying rate of interest swap. As we have been writing this text, the ten-year swap unfold was buying and selling at -26 bps. The swap charge was 4.14%, 26 foundation factors lower than the ten-year UST (4.40%).

Accordingly, the pay mounted aspect (payer) pays 4.14% yearly for ten years. In return, they obtain the day by day compounded SOFR charge. Conversely, the opposite counterparty, the receiver, will obtain 4.14% yearly and pay the day by day compounded SOFR charge. As a substitute of funds being made by each counterparties, funds are netted out. Thus, just one celebration makes a cost at every cost interval.

The cost intervals might be month-to-month, quarterly, semi-annually, or yearly. Rate of interest swaps might be tailor-made to the calls for of each counterparties. This could embody the quantity and kind of collateralization underlying the contract. Moreover, it’s frequent so as to add foundation factors to the receiving aspect of the swap to offset credit score issues. As an illustration, the settlement could have a swap unfold of -26 bps and the SOFR charge plus 12 bps.

When pricing a swap, the mounted charge is decided by calculating the ahead worth of the day by day SOFR in a single day charges over the whole swap time period. Consequently, either side are getting into right into a contract based mostly on the present market pricing of anticipated day by day in a single day charges for the following ten years.

Interest Rate Swaps: Who Makes use of Swaps And Why?

Rate of interest swaps are speculative automobiles and important threat administration instruments. We share particulars of how and why a few of the largest swap merchants use them. Nevertheless, loads of different kinds of individuals and customers exist.

Interest Rate Swaps: Speculators:

Not like shopping for a bond with money, an rate of interest swap is a by-product contract. Thus it requires solely a small quantity of up-front money or collateral. Accordingly, a speculator can successfully make a leveraged wager on rates of interest, requiring little capital.

For instance, an investor with $100 million can purchase a ten-year bond. By doing so, they’d forgo the cash market yield on the money however earn the bond return. Successfully, they may obtain the bond’s mounted charge cost and pay, by way of alternative price, the cash market yield.

Alternatively, as a substitute of utilizing money, the investor can enter a swap settlement to obtain a ten-year mounted yield and pay the floating charge. Not solely would the return profile versus the chance price (cash market charges) appear like the cash-bond funding, however after posting a small quantity of collateral, the speculator would nonetheless have a lot of the $100 million to put money into one thing else. They may additionally publish the whole $100 million of money as collateral and enter right into a a lot bigger rate of interest swap settlement. Doing so would give the investor rather more publicity to bond yields.

As a result of inherent leverage in swaps, many speculators favor rate of interest swaps over bonds. The advantage of leverage additionally helps clarify why some traders purchase swaps at a adverse swap unfold.

Interest Rate Swaps: Company Treasurers:

Companies use rate of interest swaps to transform floating-rate debt funds into long-term mounted funds synthetically. For instance, an organization enters a pay-fixed charge/receive-floating-rate swap contract. Alongside the settlement they may subject floating-rate debt or a sequence of short-term bonds matching the floating-rate element of the swap.

The floating-rate debt makes them a floating-leg payer, offsetting the obtain floating portion of the swap. What’s left is the pay-fixed leg of the swap. The sequence of transactions successfully transforms floating-rate debt into fixed-rate debt.

Since credit score threat will increase with time, most firms can borrow extra cheaply and discover higher liquidity for shorter-maturity paper. Thus, a swap mixed with a sequence of short-term debt issuances, or a floating-rate bond, permits them to benefit from short-term market pricing but lock in a set charge for an prolonged interval.

Banks/Curiosity Charge Threat Administration:

Banks are among the many most energetic customers of rate of interest swaps. Their threat administration groups continuously intention to match the length of their fixed-rate belongings (loans and fixed-income securities) with the length of their debt and deposits. On condition that banks have a tendency to make use of 10x leverage or extra, length mismatches between belongings and liabilities can introduce substantial rate of interest threat.

As an illustration, a financial institution with a weighted common length of 5 years on its belongings and three years on its liabilities is working a two-year length hole. To assist shrink the hole, the financial institution may enter right into a five-year pay-fixed and obtain floating-rate swap. Paying the mounted charge is the equal of shorting the bond market. Thus, they’re decreasing the length of their belongings and, subsequently, closing the length hole.

As an apart, whereas rate of interest swaps assist handle rate of interest threat, Credit score Default Swaps (CDS), a subject for an additional article, assist banks and others handle credit score threat.

Why Are There Unfavorable Swap Spreads?

With an appreciation for rate of interest swaps and a few motivations driving essentially the most distinguished gamers to make use of them, let’s talk about why swap spreads are at the moment adverse. To reiterate, the swap unfold is the distinction between the longer-term mounted leg of the commerce and an equal length Treasury observe or bond.

The graph under reveals that the ten-year swap unfold is at its most adverse stage within the final 5 years. Why ought to the pricing differ by that a lot if the credit score threat and rate of interest threat of rate of interest swaps and U.S. Treasuries are very related?

Unfavorable Unfold Narratives

Right now, there are three widespread narratives that we consider are the predominant forces accounting for the adverse unfold:

- Liquidity/Regulatory

- Deficits

- Speculators Looking for Length

Liquidity

Banks should maintain capital towards bond holdings. Thus, when liquidity turns into scarce in risky markets, they’re extra doubtless to purchase or promote rate of interest swaps versus bonds, because the publicity and influence on their revenue statements are related, however the capital necessities are much less onerous.

Furthermore, it’s typically simpler and less expensive to make a big commerce within the swaps market than within the bond market.

In Swaps And Basis Trades Warn Of Mounting Liquidity Problems we wrote:

Banks are pressured to promote Treasury securities to boost wanted capital, i.e., enhance their liquidity. Doing so creates a length mismatch between their belongings and liabilities. Due to this fact, to handle rate of interest dangers, they enter into rate of interest swap agreements to keep up the length of their belongings. Because the demand to obtain the mounted charge mounts, the swap charge (charge on the fixed-rate leg of the swap) trades decrease. Right now, it sits under Treasury charges, thus at a adverse unfold to Treasuries.

Resulting from capital necessities, liquidity, and buying and selling prices, paying a premium for swaps, i.e., a adverse unfold, could make sense.

Deficits

We requested a contact at a major derivatives supplier why swap spreads have been getting extra adverse and obtained the next e mail reply:

“Everybody thinks/is aware of that the fiscal deficit will worsen. Trump’s election did nothing to dissuade that. Larger deficits…extra U.S. Treasury issuance…increased U.S Treasury yields.”

When requested about different components, he opined that his financial institution thought 90% of the swap unfold low cost versus Treasury securities was deficit-related.

Basically, our buddy believes traders are involved that increased deficits will lead to extra debt issuance. Due to this fact, traders are pushing yields on Treasury securities increased as they demand a “time period premium” to guard them from the additional provide. Swap ranges should not straight impacted by larger debt issuance.

Jeff Snyder’s Opinion – Length Shopping for

Subsequent, we watched a YouTube video of Jeff Snyder, an knowledgeable on the rate of interest swap markets. He states the next:

“All swaps inform us is that the market is strongly forecasting charges to go down and keep there. We’ve got to fill within the blanks for what that may imply, and there’s no one state of affairs which might match. This may very well be a recession, however even that may result in a number of completely different near-term outcomes which finally converge sooner or later the swap market has projected. The worldwide economic system has already moved in the way in which swaps have been pricing regardless of so many doubts – together with many who stated inflation would pressure charges ceaselessly increased.”

Jeff argues that speculators are shopping for length by way of the swap market. Whereas the mounted charge on swaps is decrease than related length U.S. Treasury yields, swap payers want little money, as we famous earlier. Thus, the advantages of the leverage greater than offset the decrease yield. Moreover, liquidity within the rate of interest swap markets is plentiful.

Abstract

Oftentimes, liquidity issues present up within the extra widespread inventory and bond markets effectively after they expose themselves in different markets, similar to rate of interest swap agreements. As we graphed, rate of interest swap spreads have declined into adverse territory for over three years.

If liquidity have been plentiful, and thus leverage low-cost and simple to achieve, why would somebody conform to obtain 26 foundation factors much less by way of a swap than a money bond?

This Post Has One Comment